5/1/18 Update: Due to changes in the new tax law, as of the 2018 tax year, some of the tax concepts detailed below may no longer be applicable. For additional information and some of the other changes brought by the new law, check out this article.

First – a few definitions for words that we often hear being confused:

- Tax Return – this is the name of the actual forms that are filed with the government at year-end. For individuals, the form is a 1040, for corporations, it’s an 1120, but either way, the form itself is the tax return

- Tax Refund – this is the money that you (may) get back after filing your tax return if the amount of tax that you paid during the year exceeds your actual calculated tax at year-end

To answer our question, we need to understand a few important concepts about how income taxes work:

- Your annual income tax is calculated each year as some tax rate multiplied by some taxable income. This seems simple enough, but don’t forget that you won’t know exactly what your taxable income is until the year ends (when you can total up all of your various sources of income)

- Income taxes are due to the IRS throughout the year, either through withholding from your paycheck or by quarterly estimated tax payments, not just at year-end

You might be thinking that this doesn’t make sense! How can I be expected to pay my taxes to the IRS throughout the year if I won’t actually know how much my tax liability is until year-end? The short answer – you estimate. You estimate what you expect your tax liability to be at year-end, then you pay it in periodically over the course of the year. When you file your tax return at year-end and determine your exact tax liability, you either overpaid when you estimated (and get a refund) or you underpaid when you estimated (and have a balance due).

Two different answers for two types of taxpayers

From here, each question we ask will tend to have two answers, and which answer applies to you will depend on whether you are an employee (and have taxes withheld from your paycheck) or you are self-employed (and do not have taxes withheld on your behalf). The two parts of this post will follow the same path, but Part 1 will focus on employees with withholding, and Part 2 will look at self-employed taxpayers who do not have withholding.

Part 1 –Taxpayers Who Are Employees

You said I pay my taxes in throughout the year. How are those payments actually made?

A portion of each paycheck is withheld by your employer and paid to the IRS on your behalf. When you get a Form W-2 (from your employer) at year-end it will show both how much you earned and how much tax was withheld on your behalf.

How do I know how much to withhold?

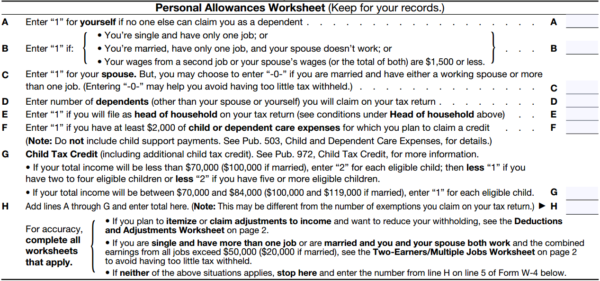

The amount withheld by your employer is most likely based on a form called a W-4, which you probably completed when you started working.

Form W-4 does its best to estimate your year-end tax liability based on a variety of factors, each of which has the effect of decreasing your tax liability. The factors it uses include things like:

- Your filing status (single, married filing joint, etc.)

- How many dependents you have

- If you have other itemized deductions (e.g. mortgage interest, state taxes, charitable donations)

The form takes all of those factors and applies them to your salary (which your employer knows) and estimates how much tax to withhold to get your estimated amount paid as close to your actual tax (determined at year-end) as possible.

I filled out a W-4 and had tax withheld, but I still got a refund at year-end. What gives?

Various factors could have caused you to be overpaid, including:

- Your deductions were higher than expected

- You got a bonus and your employer withheld tax at a higher rate (a common practice) than the rate determined by your W-4

- Your paycheck went down during the year, dropping you into a lower tax bracket

- Your tax situation changed during the year (you got married, had a child, etc.)

I filled out a W-4 and had tax withheld, but I owed money at year-end. What was different for me?

Various factors could have caused you to be underpaid, including:

- Your deductions were lower than expected

- You had fringe benefits (e.g. auto, shareholder health insurance) added to your W-2 that was not withheld against

- Your paycheck went up during the year, bringing you into a higher tax bracket

- You had income from non-W-2 sources, such as dividend or interest income, capital gains, or tax refunds from prior years

- You are being under-withheld by your employer – this is an important (and relatively common) issue to address

But if I filled out the form correctly, why would I still be under-withheld by my employer? Blame the form…

- The W-4 has been around for a long time, and when it first came to be, it was relatively uncommon for a household to have more than one person working full-time. Because of this, the form’s calculation does not do a good job accounting for multi-income households

- When the form is determining how much you should withhold, it looks at your salary to determine your tax bracket. However, it doesn’t know if your spouse is also earning a salary, which could push you into a higher tax bracket and cause you to phase out of certain deductions, exemptions, or credits

My spouse and I both work. What should we do to minimize our chances of being under-withheld?

There are two approaches that you may be able to take to avoid under-withholding:

- If your HR department will accommodate it, request a specific dollar amount to have withheld from your paycheck. For example, instead of (or in addition to) filling out a W-4, simply tell your HR department that you want $X (or X%) withheld from each paycheck. You can base your withholding amount (or %) on your prior year’s underpayment or by working with your accountant to project out your income and tax liability

- If you have to (or want to) use Form W-4 as is, you should do the following:

- Higher earning spouse – Fill out the W-4 and indicate that you do not have any dependents, including yourself. You may hear this referred to as ‘Single 0’. This will lead to the W-4 indicating the highest withholding rate

- Lower earnings spouse – Fill out the W-4 accurately using your actual marital status, number of dependents, etc

- You can also utilize the IRS’ withholding calculator, available at https://www.irs.gov/individuals/irs-withholding-calculator

In conclusion… why do I get a tax refund?

The short answer – you get a tax refund because you pay your tax during the year based on your best estimate for what your tax will be at year-end, but your estimate – and the tools used to generate the estimate – isn’t perfect, and you ended up paying in more during the year than was actually necessary.

And do I really want one?

Unless you are someone who relies on the “forced savings” that a tax refund provides, no, you don’t want a tax refund. Getting a refund is effectively giving the government an interest free loan, and you would have been better off taking home a higher paycheck all year and not getting a refund at year-end. That said, unless the refund is large, it is probably not worth the cost or time it would take to prepare annual projections and adjust your withholding accordingly, but small tweaks to your withholding (by submitting an updated W-4 to your HR department) are a good way to keep your withholding in line and keep your refund (or underpayment) to a minimum.

In Part 2 we will take a look at the same set of questions, but we will answer them for a taxpayer who is self-employed and does not have a salary with tax withheld from their paycheck.

Note: This article was intended to provide a high-level introduction to withholding, estimating and projecting personal income taxes. In practice, this topic can be extremely nuanced and vary from situation to situation. We strongly recommend consulting a tax advisor (like us) when doing any tax planning.