In general, there are a few “standard” ways to save for your retirement:

- Traditional retirement accounts (contributions to these accounts can be deductible or non-deductible, but for the purposes of this article we’re talking about deductible contributions)

- Roth retirement accounts

- ???

These retirement accounts can be in the form of a 401k (through your employer), a 403b (such as if you’re an educator), an IRA (if you set up the plan for yourself), as well as others. For this article, we’ll be talking about IRAs.

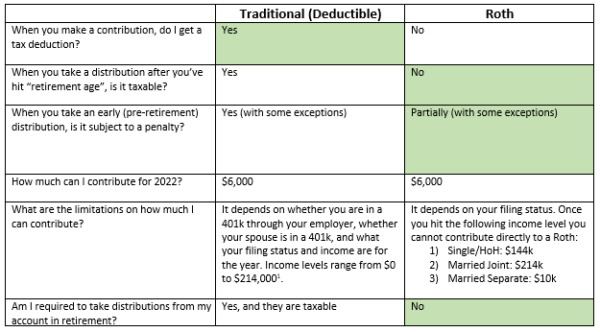

Traditional vs. Roth

These two types of retirement accounts vary significantly in many ways, such as how much you can contribute, what deduction you get, and how you get taxed. One key similarity is that the funds in the account will grow tax-free (meaning interest, dividends, and capital gains earned on funds held in the account will not incur any tax).

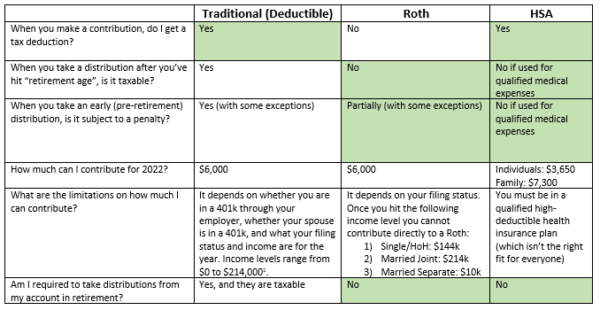

Secret Option Number Three

Secret option number three is your Health Savings Account (i.e. your HSA). Yes, this is a savings account that is designed to be used to pay for health expenses pre-tax, however, because of the way it’s set up, you would be better off contributing, but not spending, funds in your HSA for as long as you can. Let’s quickly look at what an HSA offers:

What else should I know?

- You can save the funds in your HSA for when you’re retired (and likely have more medical expenses) and use them then, after they’ve grown tax-free between now and your retirement. The interest, dividends, and capital gains are not taxed when earned (just like in an IRA), and the distributions used for medical expenses are not taxable!

- Worried you won’t have enough medical expenses in retirement to use up your HSA funds? You can stockpile receipts for your medical expenses starting now, save them in a Dropbox folder for the next 30 years, and then take reimbursements from your HSA whenever you want based on these receipts. There is no time limit that says you must be reimbursed from your HSA for medical expenses within X months or years, so you can literally save a receipt from a prescription you picked up this morning and use it to support a distribution you take from your HSA in 2050. I keep mentioning receipts because it is important that you have backup to support your reimbursements in case of audit, especially if you’re going to wait several years (or decades) and take a big distribution all at once.

- You don’t have to wait for retirement to take these funds out (but the longer they live in the HSA the longer they enjoy tax-free growth). If you have the receipts to support your distribution you can take out the funds whenever you want, tax free

- If you qualify to contribute to a traditional or Roth IRA, you can do an HSA contribution on top of these (and/or on top of your 401k)

- If you withdraw funds from your HSA and use them for non-qualified expenses, the distribution will be subject to income tax. If you haven’t yet hit retirement age, the non-qualified distribution will also be subject to a penalty. Note that if you have hit retirement age, the distributions act just like distributions from a traditional IRA (taxable but no penalty)

- You have to have the cash flow to support funding your HSA and paying your medical bills out of a different account. If you don’t have the cash flow for that right now, then you can still benefit from an HSA by making deductible contributions and using the HSA balance to pay your qualified medical expenses

Conclusion – The Best of Both Worlds

The HSA gives you the best of the traditional and Roth IRA accounts, plus more, if used correctly (i.e. the funds are just left in the HSA and invested, not spent). To recap:

- Deductible contributions

- Non-taxable distributions (if used for qualified medical expenses)

- Can contribute to an HSA in addition to other retirement accounts

- No penalties for “early” withdrawals (if used for qualified medical expenses)

- No required minimum distributions (RMDs)

Footnotes

- For details on the phase-out levels for deductible IRA contributions, see this IRS page: https://www.irs.gov/newsroom/irs-announces-changes-to-retirement-plans-for-2022

This is a complex and nuanced area of the tax code. Always consult your tax adviser before making any tax planning decisions.