September 16

– Filing deadline for extended 2023 calendar-year S corporation and partnership tax returns

– 3rd quarter installment of 2024 estimated income tax is due for individuals, calendar-year corporations and calendar-year trusts & estates

October 15

– Filing deadline for extended 2023 individual and C corporation tax returns

Reducing the amount of interest you pay over the life of a mortgage can yield huge savings! This month’s newsletter provides an illustration of just how much you can save, even with as little as $10 a month.

Also in this edition, find out how cancelled debt may leave you holding a bigger tax bill, why banks won’t always come to the rescue if you get scammed, and how to protect your valuables before thieves decide to pay your home or apartment a visit.

As always, feel free to pass this information on to anyone that may find it useful and please call if you have any questions or concerns.

Banks Won’t Always Save You from Scams

It’s easy to feel secure about the money you deposit with a bank you’ve come to trust. After all, most banks and credit unions offer certain levels of protection against fraudulent transactions.

Banks, however, won’t protect you against all types of fraud.

Here’s a look at the protections that banks and credit unions usually provide to their customers – and which situations where you’ll likely be on your own.

When a Bank Usually Protects You

For credit cards, banks usually provide zero liability on any unauthorized charges.

Debit cards also provide protection against fraudulent purchases, but there may be limitations depending on which financial institution issued your card. According to federal law, here is the maximum amount of fraudulent transactions you’ll be responsible for depending on when you notify your bank that your card is lost or stolen:

- Immediately notify your bank before any unauthorized charges are made: Zero liability

- Within two business days: Up to $50

- After two business days but within 60 days: Up to $500

- Fail to notify within 60 days: Unlimited

When a Bank Usually WON’T Protect You

Unfortunately, there are many types of scams that banks won’t reimburse you for if someone steals your money. Here are some of the more common scams:

- You are scammed into moving money out of your account and into another person’s account.

- A hacker uses lies to convince you to make a bank transfer into a cryptocurrency wallet.

- You liquidate your retirement funds and send the money to someone else for any reason, even if you were conned into it.

- You make a person-to-person transfer to another individual using an online payment app, and that transfer doesn’t come with any type of purchase protection.

How to Protect Yourself from Common Banking Scams

Here’s how to protect yourself from getting scammed:

- Don’t communicate about your accounts unless you initiate the conversation. If someone calls about your bank account, hang up and call the financial institution directly using your normal means of contact.

- Never share your information. Don’t share account details or personal information online or over the phone, especially if you were asked to share these details in a phone call you didn’t initiate or via email.

- Tell someone. Scammers try to isolate you from family members and friends. If you’re unsure about a banking transaction you plan to make, or you wonder if you’re being victimized, tell someone you trust about the situation.

- Ask your bank for help. Bank tellers are trained to spot the early signs of fraudulent transactions. If you’re making a bank transfer and feel unsure about the situation, explain it to a teller or bank representative and ask for their help.

- Report the incident. Whether you unfortunately got scammed or you spotted the attempted scam before withdrawing any money, submit a report of the situation by visiting ReportFraud.ftc.gov.

Early Mortgage Payoff: Small Payments Can Save You Big Money

Small payments can save you big money when paying off your mortgage.

With 30-year fixed rates reaching levels not seen in 25 years, adding even just a little extra to your monthly payment can significantly cut down on the interest you pay over the life of your mortgage.

Here are several different scenarios to illustrate how much interest you can save by slightly increasing each monthly payment.

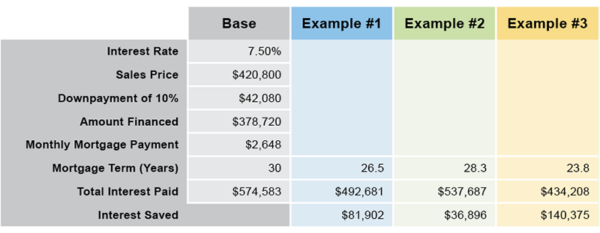

Base scenario and assumptions

Here’s the assumptions used for this base scenario:

- Average U.S. home price ($420,800) and mortgage rate (7.50%) for early 3rd quarter of 2024

- Average U.S. downpayment of 10%

- House financed using a 30-year fixed rate mortgage

- Monthly payment includes principal and interest payments only; it does not include other expenses typically bundled with monthly payments, such as property taxes, homeowners insurance, and mortgage insurance premiums

With no additional money tacked on to your monthly payment, you would pay $574,583 in interest over the course of your 30 year mortgage in this base scenario.

To buy this house for $420,800, you would end up paying just shy of $1 million after adding $574,583 of interest charges!

None of us wants to pay $1 million for a $420,000 house. So let’s take a look at the following scenarios to find out how much interest expense you can save by increasing your monthly payments by a small amount.

Here’s a summary of the base scenario’s assumptions compared with how much interest you can save, and how much faster you’ll pay off your mortgage, in each of the following examples.

Example #1: An Extra $100 Per Month

Adding an extra $100 to your monthly mortgage payment would save you $81,902 in interest expense and cut down on the time to pay off your mortgage by 3½ years.

Example #2: An Extra Lump-Sum at Years 5, 15 & 25

In this example, let’s assume you make an additional lump-sum payment of $5,000 in years 5, 15, and 25 of your mortgage.

While you wouldn’t save that much extra time paying off your mortgage in this scenario, you’ll still end up pocketing nearly $37,000 just by making three lump-sum payments over the course of your mortgage.

Example #3: An Extra $200 Per Month

If you can afford an extra $100 per month to put towards your mortgage, why not try for $200 a month? This is where the math starts to get fun. Adding $200 a month helps pay off your mortgage 6 years sooner and saves you $140,000 in interest expense.

Every little bit helps

Even adding an extra $10 per month can save you nearly $10,000 over the course of your mortgage. That’s a lot of money that goes into your bank account instead of your bank’s bank account!

Paying off your mortgage early and cutting down how much interest you pay over the course of your mortgage doesn’t require a lot of money. Whether it’s $100 or $10 a month, every little bit can help on your quest towards a better financial future for you and your family.

Debt Relief and Taxes

What everyone should know

Negotiating to decrease or zero out a credit card bill or other loan balance can help relieve a tough financial situation, but it can also give way to an unexpected tax bill. Here’s a quick review of various debt cancellation situations and how they impact your your taxes.

- Consumer debt. If you have a credit card balance or loan forgiven, be prepared to receive IRS Form 1099-C representing the amount of debt cancelled. The IRS considers that amount taxable income to you, and they expect to see it reported on your tax return. However, if you’ve filed for bankruptcy or have liabilities that exceed your assets, then you may not need to report a cancelled debt as taxable income.

- Primary home. If your home is short sold or foreclosed and the lender receives less than the total amount of the outstanding loan, expect that amount of debt cancellation to be reported to you and the IRS. But special rules allow you to exclude up to $2 million in cancellation income in many circumstances. You’ll need to fill out paperwork to report this special homeowner exclusion to the IRS, but the end result can be a generous tax break for you and your family.

- Student loans. While this topic has generated plenty of recent headlines, the basics of student loan forgiveness have remained essentially the same. If your school closes while enrolled or soon after you withdraw, you may be eligible to discharge your federal student loan and not include the forgiven amount as taxable income. And if you are able to take advantage of the recent student loan forgiveness provision under the American Rescue Plan Act of 2021, your cancellation may be exempt from federal tax. The challenge, though, is that recent forgiveness programs are still being challenged in court AND your state may still wish to tax the loan forgiveness.

- Second home, rental property, investment property, & business property. The rules for debt cancellation on second homes, rental property, and investment or business property can be extremely complicated. Given your cost of these properties, your financial condition, and the amount of debt cancelled, it’s still possible to have this debt cancellation taxed at a preferred capital gains rate, or even considered not taxable at all.

Each of these themes have one thing in common – the tax laws can be complicated and you will probably need help navigating your situation.

Protect Your Valuables BEFORE Thieves Arrive

If you are concerned about protecting your valuables, here are several suggestions to consider for protecting them from would-be thieves:

- Rent a safe deposit box. It may make sense to keep seldom worn jewelry, coins and other important documents in a traditional safe deposit box at your local bank. But beware if you go this route, as it’s often inconvenient to retrieve your valuables, as well as easy to forget what is in the box and who has the key. Plus it’s important to fully understand your rights under the contract terms.

- Install a home safe. There are several types of in-home safes you can choose from, including wall, floor, free standing, fire and gun safes. There are also diversion safes for small items that are designed to look like everyday household objects that can blend in with its surroundings.

- Secure your house. In addition to installing a state-of-the-art home security system, there are several other ways to physically secure your home. Consider updating your locks every several years, and remember to actually use them! Many burglars are looking for easy targets, and unlocked doors and windows provide easy access. Also consider reinforcing your doors and windows, and installing motion-sensing lights both inside and outside.

Be prepared if a theft does occur

Thieves can still unfortunately steal your valuables despite multiple layers of protection. Here are some suggestions to prepare you if any of your valuables go missing:

- Be familiar with your insurance policy. Read your insurance policy to know what items are covered. Review your policy once a year or whenever you acquire another valuable asset.

- Get an appraisal. It may be difficult to know how much insurance you need without a proper valuation of your assets. Some assets may be worth much more than you think, while other assets may be difficult to pinpoint a value without professional assistance.

- Keep a home inventory. Create a list of all your valuables that includes photographs and purchase receipts. If an asset is stolen, having an up-to-date inventory list and documentation can help quickly jump-start filing an insurance claim.