September 15

– Filing deadline for extended 2022 calendar-year S corporation and partnership tax returns

– 3rd quarter installment of 2023 estimated income tax is due for individuals, calendar-year corporations and calendar-year trusts & estates

October 16

– Filing deadline for extended 2022 individual and C corporation tax returns

With interest rates continuing to increase, what could be better than making a purchase with 0% interest? In reality, financing a purchase with a 0% interest rate may be more trouble than it’s worth, as we explain in this month’s newsletter.

Also discover the hidden tax benefits of owning a home, how students and teachers can sharpen their AI toolkit for the upcoming school year, and where you can find a savings account with a great interest rate.

As always, please pass this newsletter to anyone who may find it valuable and call if you have any questions or concerns.

The Trouble With 0% Financing

Companies want to make it easy to buy their big ticket items, especially at times of economic uncertainty. A popular technique is to offer 0% financing when you buy furniture, electronics and other household items. You can also take matters into your own hands with a credit card that offers 0% APR on purchases, balances transferred to the card, or both.

While paying for goods and services with 0% interest may sound appealing, there are risks you’ll face that you should be aware of before you take this step.

What’s hiding behind 0% financing

Here are some of the potential problems hiding behind these 0% financing offers:

- Special financing offers make it easier to overspend. Psychology Today reported that credit card use can easily result in overspending, and the same is true for loans. The key is to understand the monthly payments you are committing to, and ensuring you can handle them. At the same time, try to assess your purchase decision. Would you buy this item if the 0% offer was not available?

- Some 0% APR offers come with deferred interest. Hidden in the fine print of some 0% interest offers may lurk deferred interest charges. This means that while you’re enjoying monthly payments with no interest, the interest charge accrues over time. If you miss a payment, have a late payment or haven’t paid off the loan by the end of the 0% offer period, the accrued interest gets added to your unpaid balance. The key is to precisely understand what happens if you miss a payment or don’t follow the 0% offer exactly as written…before you take the 0% offer.

- The 0% offer may be impacting the price. Remember, money has value and someone is paying the interest cost of the 0% financing. Usually the merchant is hiding the cost inside the price you are paying for the item.

What you can do

Before considering a 0% interest financing offer on your next purchase, do this:

- Save up for large ticket purchases. Instead of financing items and ensuring you have even more bills to pay each month, start saving for pricier purchases on a regular basis. Even better, leverage the value of your savings within higher interest savings account options that are now in excess of 4 percent.

- Turn on your negotiating switch. Whenever you see a 0% offer, there should be a discount available to you for paying upfront. Someone is paying the interest and it is probably going to be you if the financing cost is built into the price you are paying.

- Pay on time! Finally, if you do think the 0% option is a deal for you… set up auto payments. Most of these deals are unforgiving and punitive if you miss a payment, so automate them to avoid this possibility.

Your Home is a Bundle of Tax Benefits

There are many tax benefits built into home ownership. Here is a review of the most common.

- The home gain exclusion. When you sell an asset for a profit, it creates a taxable event. If the asset, though, is your primary residence, you can exclude up to $250,000 ($500,000 if married filing jointly) of these gains. Special rules do apply, but this is a major tax benefit of home ownership.

- How to take advantage: You must live in your house for at least 2 of the previous 5 years to qualify for the home gain exclusion. Start planning now if you think you’ll be selling your house in the near future so you can qualify for this tax break.

- Itemized deductions. Mortgage interest and property taxes are two deductions you can claim as a homeowner. The interest is deductible on the first $750,000 associated with loans secured by your primary and secondary residences ($1 million for mortgages underwritten prior to 2018), while up to $10,000 of property taxes may be deducted. You may also deduct points paid as an itemized deduction over the life of your mortgage.

- How to take advantage: You need to itemize your deductions to take advantage of these tax breaks. Consider bunching your mortgage interest and property taxes with other itemized deductions such as charitable contributions, taxes and excess medical expenses to try and exceed the standard deduction for your filing status.

- Free rental income. You can rent out your home for up to two weeks and not claim the income. While you cannot deduct expenses in this scenario, this is a great tax break if your home is located next to a popular landmark or a major event.

- How to take advantage: Keep track of how many days you rent out your home so you don’t go over the 14-day limit. If you rent your house for just 15 days over a given year instead of 14, you’ll owe taxes on all rental income for that year, including the first 14 days.

- Home office deduction. If you use a portion of your house exclusively as a home office, you may be able to deduct certain expenses such as mortgage interest, insurance, utilities, & repairs.

- How to take advantage: To qualify for the deduction, you generally must use this portion of your house exclusively for business purposes on a regular basis. So be sure to understand the limitations of this deduction.

Your house is a great place to control the amount of tax you owe, but only if you know the rules and can apply these rules to your situation. Use this information as a starting point to see if there are ways to leverage your home’s tax benefits.

Sharpen Your AI Toolkit for the Upcoming School Year

Artificial intelligence got pushed front and center in America’s classrooms with the release of ChatGPT in late 2022. As a new school year gets underway, here are some ideas for both students and teachers to harness the power of AI in the classroom.

AI Tips for Students

- Get personalized feedback. Real-time feedback can help students master a subject in a shorter amount time and provide learning recommendations based on that student’s strengths and weaknesses.Consider this app: Cognii gives students real-time feedback on assignments and uses conversational technology to help students learn at a quicker pace.

- Learn with simulations. Using simulations and gamification to learn a complicated subject can help reinforce critical thinking skills while mastering difficult areas such as STEM subjects.Consider this app: Querium provides personalized short-form lessons and practice tests in STEM subjects. The app also has a virtual tutor that gives targeted support when needed to keep a student on track.

- Understand the Why. Technology can help you quickly find or calculate an answer, but it’s also important to understand the why behind an answer. AI can not only help you find the answer to a question or a problem, but also explain to you why that answer is the correct answer.Consider this app: Carnegie Learning uses adaptive learning to re-create the human tutoring experience while helping students understand a subject’s underlying concepts.

(Article continues below survey results)

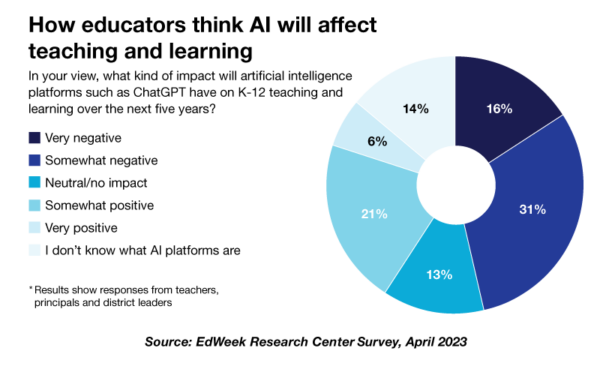

| How educators think AI will affect teaching and learning

In your view, what kind of impact will artificial intelligence platforms such as ChatGPT have on K-12 teaching and learning over the next five years?

* Results show responses from teachers, principals and district leaders. Source: EdWeek Research Center Survey, April 2023 |

AI Tips for Teachers

- Delegate administrative tasks. Teachers work an average of 54 hours a week, but only spend 25 hours directly teaching students, according to the 2022 Merrimack College Teacher Survey. Automating time-consuming tasks such as generating progress reports or drafting emails can help you focus on what really matters – spending more direct time teaching your students.Consider this app: Fetchy has more than 50 tools, such as list generation, organizational tools, text reminders, and an AI advice engine to help teachers stay on top of their daily tasks.

- Get help with grading. Another time consuming task for teachers is grading. AI can act as a grading assistant by providing a draft score for an assignment. You can then review these draft scores and make any adjustments before finalizing the grade.Consider this app: Gradescope helps teachers grade assignments quickly and consistently while still allowing for detailed feedback. This app can tackle math, computer science, physics, economics and more in all types of formats including paper-based, digital and code assignments. The goal is to cut your grading time in half!

While most of the information in the news regarding AI is about how to avoid writing your own papers, AI if applied correctly can be used to save time while enhancing the learning experience.

Take a Look at Better Savings Rates

A silver lining to continued interest rate hikes by the Federal Reserve is being able to earn more interest on cash stashed in your savings accounts. How much interest, exactly, you can earn depends on where you do your banking. Consider these tips to earn as much interest as you can, even if it means opening a new account:

- Earn a bank bonus. Some banks offer a bonus if you meet specific requirements, such as depositing a minimum amount or setting up direct deposit. These bonuses can give you an incentive to try a new bank while padding your savings with a few extra hundred dollars.

- Look beyond your local bank. If you want to earn enough interest on your savings to keep up with inflation, look beyond your local bank to the range of online banks offering much higher interest rates. For example, Chase banking customers are currently earning 0.01% on their savings, while those who save with UFB Direct are earning 5.06% APY with no monthly maintenance fees or minimum balance requirements.

- Take advantage of new banking tools.Bankrate.com shows approximately 60% of consumers are very or somewhat interested in using a digital bank in the coming year. This is partly due to the digitization of nearly all other aspects of our lives, but it’s also due to convenient online tools like mobile check deposit, virtual account management and bill pay features.

- Watch out for fees. Take note that many of the best bank accounts with great rates don’t charge monthly maintenance fees or any hidden fees. However, you’ll want to read over the fine print for accounts you’re considering so you know for sure. This is especially true with CD’s at some banks that tease with high interest rates, but hide the 1% to 3% penalties of your balance for early withdrawal.

- Stability is important. When making a banking move, double check to ensure your deposits are FDIC insured. But even if insured, you still should check the press for any indication of deposit risk at your chosen bank. And if your current bank is still offering low interest rates, it may be subject to deposit flight limits that may create difficulty removing your funds. So while your money is insured, it may be hard to withdraw should this happen.

Today’s interest rates can be a boon for your finances, but you’ll need to put in some work up front to find the best bank for your particular situation. Shop around for a new bank and look for ways to get ahead, either through banking bonuses, great rates or both. The time and effort you spend will be worth it in the end!