As 2025 starts to wind down, now’s your chance to make some strategic moves that could pay off well into next year. In this month’s newsletter, we’re focusing on key actions that can sharpen your finances as we head into the final few months of the year.

First up: a final tax planning review checklist to help you spot any last-minute opportunities to reduce your 2025 tax bill. We also break down the latest Social Security cost-of-living adjustments and how they might impact your income. Also learn about five essential financial terms that can give you an edge with managing your money.

Finally, we take a look at the rise of the DIY economy and why more people are choosing to fix, make, and create instead of just buy, and how you can be part of this movement.

Still Time to Reduce Any Tax Surprises!

Consider conducting a final tax planning review now to see if you can still take actions to minimize your taxes this year. Here are some ideas to get you started.

Review your income. Begin by determining how your income this year will compare to last year. Since tax rates are the same, this is a good initial indicator of your potential tax obligation. However, if your income is rising, more of your income could be subject to a higher tax rate. This higher income could also trigger phaseouts that will prevent you from taking advantage of certain deductions or tax credits formerly available to you.

Examine life changes. Review any key events over the past year that may have potential tax implications. Here are some common examples:

- Purchasing or selling a home

- Refinancing or adding a new mortgage

- Getting married or divorced

- Incurring large medical expenses

- Changing jobs

- Welcoming a baby

Identify what tax changes may impact you. There were lots of changes this year thanks to a new tax bill passed this summer. Here are some of the more important changes to be aware of:

- Up to $25,000 of tip income can be excluded from income

- Up to $12,500 of overtime income ($25,000 for married couples) can be excluded from income

- Increase in the standard deduction

- New $6,000 senior citizen deduction

- Child tax credit is increased to $2,200

- State and local tax deduction is increased to $40,000

Manage your retirement. One of the best ways to reduce your taxable income is to use tax beneficial retirement programs. So now is a good time to review your retirement account funding options. If you are not taking full advantage of the accounts available to you, there is still time to make adjustments.

Look into credits. There are a variety of tax credits available to most taxpayers. Spend some time reviewing the most common ones to ensure your tax plan takes advantage of them. Here are some worth reviewing:

- Child Tax Credit

- Earned Income Tax Credit

- Premium Tax Credit

- Adoption Credit

- Elderly and Disabled Credit

- Educational Credits (Lifetime Learning Credit and American Opportunity Tax Credit)

Avoid surprises. Your goal right now is to try and avoid any unwanted surprises when you file your tax return. It’s also better to identify the need for a review now versus at the end of the year when time is running out. And remember, you are not required to be a tax expert. Use the tips here to determine if a review of your situation is warranted and please call if you have any questions about your tax circumstances.

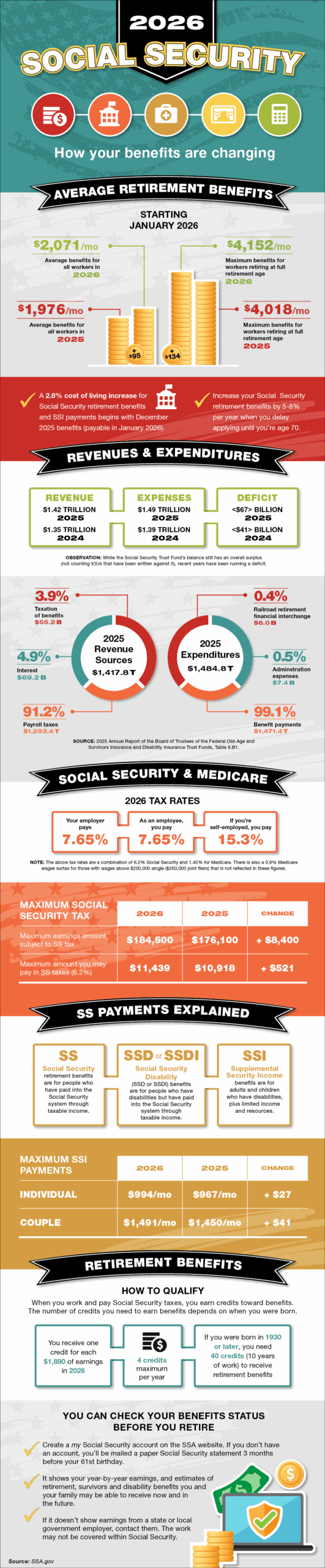

2026 Social Security Changes Announced

5 Financial Terms Everyone Should Know

Money impacts nearly every part of life. Whether you’re just starting your career, running a household, or trying to grow your savings, understanding a few key terms can give you a real advantage. Here are 5 financial terms that you should understand to help better manage your money

1) Net Worth = Assets – Liabilities

What it is: Net worth is the bottom line of your financial life. It’s what you own (assets) minus what you owe others (liabilities). The result of this math is your net worth.

Why it matters: Forget income for a second. Net worth is the real measure of how well you’re doing financially speaking. You can make six figures and still be broke if you’re drowning in debt. Tracking net worth shows whether you’re moving forward, stuck in place, or sliding backwards.

Planning tip: Watch your net worth like a financial GPS. Check in regularly. If it’s not growing, it’s time to rethink how you’re spending, saving, or investing. Consider creating this calculation at the beginning of each year, then compare it over time.

2) Compound Interest

What it is: Compound interest is like a money snowball. You earn interest not just on your original cash, but also on the interest on the interest that was made in previous time periods. It’s growth feeding on growth.

Why it matters: This is how small savings turn into serious wealth. Compound interest doesn’t just add, it multiplies. It’s the silent force behind retirement accounts, savings plans, and long-term investments. The sooner you start, the harder it works.

Planning tip: Start understanding and applying compounding NOW! It works in a bank’s favor with mortgages and credit card debt. It works in your favor with savings and retirement accounts. Actively manage it. Search bank accounts that pay reasonable interest (most don’t!). Maximize your retirement contributions. Make extra payments on credit card debt and loans like your mortgage. Even a few dollars invested early can outpace thousands invested later. Time isn’t just money, it’s compounding!

3) Liquidity

What it is: Liquidity is all about access. It’s how quickly you can turn an asset into spendable cash. A $100 bill? Instantly liquid. A house? Not so much. It takes time and effort to sell and turn a home into cash.

Why it matters: When life throws a curveball, you want money as soon as possible, not stuck in a slow-moving investment. Liquid assets give you financial agility, which is essential during emergencies or unexpected expenses.

Planning tip: Keep an emergency fund in something ultra-liquid like a savings account. That way, when things get rough, you’re not forced to sell stocks or real estate at the worst possible time.

4) Debt-to-Equity Ratio (DTE) = Total Personal Debt / Personal Net Worth

What it is: DTE compares how much debt you have to how much you own outright. Your equity is your net worth (see above), which is what’s left after subtracting your debts from your assets.

Why it matters: This number tells you if you’re living on solid ground or skating on financial thin ice. A high DTE means debt is doing the heavy lifting in your life, which is typically risky. A low DTE means you actually own most of what you have.

Planning tip: Track your DTE like a financial vital sign. Aim to lower it over time by paying down debt and building assets.

5) Loan-to-Value Ratio (LTV) = Loan Balance / Current Value of the Asset

What it is: LTV is how much you owe on a loan compared to what the asset (usually a home or a vehicle) is currently worth.

Why it matters: Lenders look at LTV to size up their risk. A low LTV means more equity and less risk for the lender – you’re likely to get better interest rates. A high LTV means you’ve borrowed most of the asset’s value, which can mean higher rates, extra fees, or even being denied a loan.

But LTV isn’t just a bank’s problem. It’s yours, too. A high LTV means you’ve got little skin in the game. If prices drop or something goes wrong (like a vehicle getting totaled), you could owe more than the asset is worth. That’s called being underwater, and no one wants to drown in debt.

Planning tip: ALWAYS keep your LTV under 80%. 50% is a safer target. The more equity you build, the more control and options you have, whether you’re refinancing, selling, or just sleeping better at night.

Financial literacy isn’t about knowing everything. It’s about understanding the basics well enough to make smart decisions. These five terms are your starting blocks. Get familiar with them and you’ll be able to build a stronger financial future.

The Rise of the DIY Economy – And How You Can Participate

We used to fix things. Then came mass production and making gave way to buying. But something’s shifting. Again.

Welcome to the rise of the DIY economy. Here’s a look at what’s driving this shift and how you can participate.

The solution is at your fingertips

You no longer need a workshop full of specialized gear to be a maker. A $300 3D printer can produce functional parts at home. A smartphone can film a tutorial that hits a million views by midnight. Online platforms are modern-day apprenticeships. Want to fix something? There’s a tutorial for that, and probably one will help get the job done.

Creativity meets commerce

Once the tools became universally accessible, it was just a matter of time before DIYers figured out how to turn a passion project into a business. Internet sites make it simple for creators to sell directly to consumers, with no middlemen. For many, the DIY route isn’t just about extra cash. It’s about independence, creative control, and ownership.

The downside of DIY

The DIY economy isn’t a perfect system, though. Turning a hobby into a business can sometimes suck the joy out of it. When your income depends on constantly creating, the pressure can be intense. Platform dependence is also risky. Many maker businesses rely on algorithms, trends, and third-party platforms. One change in a selling site’s policy and revenue can vanish overnight.

Ideas to jump into DIY

Whether you’re itching to create something or just looking for more control over how you earn and live, there’s a place for you in the DIY economy.

- Start small. Pick one area of your life to DIY. It could be fixing your own clothes, learning basic bike repair, or cooking a meal.

- Learn a new skill. Set aside an hour a week to learn something new: 3D modeling, woodworking, knitting, canning, coding, or sewing. The ideas are endless.

- Join a maker community. Look for makerspaces in your area, or join online forums that match your interests. Sharing progress, asking questions, and seeing others’ work will push you further than going solo.

- Sell something simple. Got a handmade item, print, or digital file someone might want? List it on a marketplace. Test the waters before plunging into the deep end of the pool.

- Fix first, buy later. Next time something breaks or wears out, ask: Can I repair this? Can I remake it?

- Treat your time like it matters. DIY doesn’t always mean doing everything yourself. Sometimes it means building systems, automating tasks, or learning just enough to delegate wisely.

The rise of the DIY economy isn’t just about saving money or passing time. It’s about control, connection, and identity. And because it feels better to create than to consume. Enjoy the journey!