The new year is upon us and so is another tax filing season.

With all the late breaking tax law changes, advance payments of the child tax credit, and several stimulus payments, this year’s tax return may be a bit chaotic. But your situation does not have to be. Included in this month’s newsletter are some tips to help your tax journey be a smooth one.

Also included is a great reminder for all of us to be prepared in case of fire. With the busy nature of our lives, this is an area that can be easily overlooked. There are also timely updates to retirement plan contribution limits for 2022 and a great list of ideas to help your small business prepare for the upcoming tax season.

Please enjoy the information, and pass along articles of interest to all your family and friends. And as always, please call if you have questions or need help.

Make Order Out of Chaos

Prepare for this year’s tax return filing season

Tax return filing season usually gets a little crazy, but this year will be more turbulent than most. Due to new tax legislation and guidance from the IRS, you will have to cope with a wide variety of tax changes, some of which relate to the pandemic. Here are several tips for making some order out of the chaos.

Unemployment benefits

Unemployment benefits are taxable once again in 2021. In 2020, the first $10,200 of benefits received by taxpayers with an adjusted gross income (AGI) of less than $150,000 were exempt from tax. Unfortunately the tax-free nature of unemployment benefits in 2020 was made long after many of you filed your tax return. If this pertains to you, and you haven’t received a refund from a tax overpayment yet, you might need to file an amended 2020 tax return.

Small business loans

To kick start the economy during the pandemic, Congress created a loan program called the Paycheck Protection Program (PPP). Similarly, your small business might have received an Economic Injury Disaster Loan (EIDL) or grant. These loans may be forgiven in 2021 without any adverse tax consequences if certain conditions were met. So gather your records—including what you received and when—for optimal tax protection.

Economic impact payments

Congress handed out three rounds of Economic Impact Payments to individuals in 2020 and 2021. The third payment provided a maximum of $1,400 per person, including dependents, subject to a phaseout. For single filers, the phaseout begins at $75,000 of AGI; $150,000 for joint filers. So review your records and be very clear what payments you received in 2021. Only then can you use your 2021 tax return to ensure you receive credit for your full stimulus payments.

Child tax credit

Many families will benefit from an enhanced Child Tax Credit (CTC) on their 2021 tax return. The new rules provide a credit of up to $3,000 per qualifying child ages 6 through 17 ($3,600 per qualifying child under age six), subject to a phaseout beginning at $75,000 of AGI for single filers and $150,000 for joint filers. What will complicate this year’s tax filing are any advance payments you received from the IRS during the second half of 2021. It is important that you accurately identify all the payments you received. Only then can correct adjustments be made on your tax return to ensure you receive the full Child Tax Credit amount.

Dependent care credit

The available dependent care credit for qualified expenses incurred in 2021 is much higher than 2020, with a corresponding increase in phaseout levels. The maximum credit for households with an AGI up to $125,000 is $4,000 for one under-age-13 child and $8,000 for two or more children. The credit is gradually reduced, then disappears completely if your AGI exceeds $440,000.

Due to the ongoing debate of proposed legislation in Washington, D.C., this year’s tax filing season will seem a bit chaotic. With proper preparation, though, your situation can be orderly…but only if you prepare!

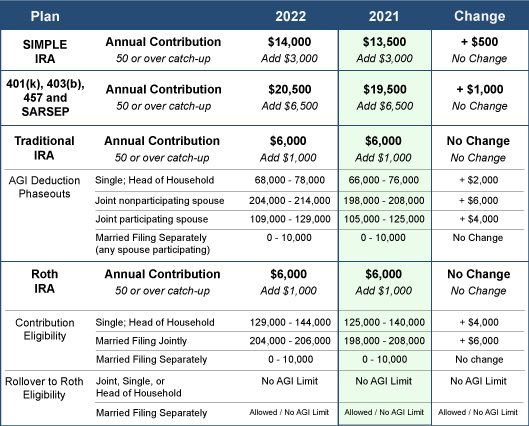

Plan Your Retirement Savings Goals for 2022

There’s good news for your retirement accounts in 2022! The IRS recently announced that you can contribute more pre-tax money to several retirement plans in 2022. Take a look at the following contribution limits for several of the more popular retirement plans:

What You Can Do

- Look for your retirement savings plan from the table and note the annual savings limit of the plan. If you are 50 years or older, add the catch-up amount to your potential savings total.

- Then make adjustments to your employer provided retirement savings plan as soon as possible in 2022 to adjust your contribution amount.

- Double check to ensure you are taking full advantage of any employee matching contributions into your account.

- Use this time to review and re-balance your investment choices as appropriate for your situation.

- Set up new accounts for a spouse and/or dependents. Enable them to take advantage of the higher limits, too.

- Consider IRAs. Many employees maintain employer-provided plans without realizing they could also establish a traditional or Roth IRA. Use this time to review your situation and see if these additional accounts might benefit you or someone else in your family.

- Review contributions to other tax-advantaged plans, including flexible spending accounts (FSAs) and health savings accounts (HSAs).

Now is a great time to make 2022 a year to remember for retirement savings!

Small Business Tax Return To-Do-List

Eight ideas to make filing your tax return easier

Consider these suggestions for helping to make tax season smooth sailing this year for your small business:

- Make your estimated tax payments. Tuesday, January 18th is the due date to make your 4th quarter payment for the 2021 tax year. Now is also the time to create an initial estimate for first quarter 2022 tax payments. The due date for this payment is Monday, April 18.

- Reconcile your bank accounts. Preparing an accurate tax return starts with accurate books. Reconciling your bank accounts is the first step in this process. Consider it the cornerstone on which you build your financials and your tax return. Up-to-date cash accounts will also give you confidence that you’re not over-reporting (or under-reporting!) income on your tax return.

- Organize those nasty credit card statements. If you use credit cards for your business, develop an expense report for these expenditures, if you have not already done so. The report should recap the credit card bill and place the transactions in the correct expense accounts. Attach actual copies of the expenses in the credit card statement. You will need this to support any sales tax paid in case of an audit. Use this exercise to show you are only including business-related expenses by reimbursing your business for any personal use of the card.

- Reconcile accounts payable. One of the first tax deadlines for many businesses is issuing 1099 forms to vendors and contractors at the end of January. Get your accounts payable and cash disbursements up-to-date so you have an accurate account of which vendors you paid.

- Get your information reporting in order. Now identify anyone you paid during the year that will need a 1099. Look for vendors that are not incorporated like consultants or those in the gig economy and don’t forget your attorneys. You will need names, addresses, identification numbers (like Social Security numbers) and amounts billed. Send out W-9s as soon as possible to request missing information.

- File employee-related tax forms. If you have employees, file all necessary W-2 and W-3 forms, along with the applicable federal and state payroll returns (Forms 940 and 941). Do this as soon as possible in January to allow time to identify any potential problems.

- Compile a list of major purchases. Prepare a list of any purchases you made during 2021 that resulted in your business receiving an invoice for $2,500 or more. Once the list is compiled, find detailed invoices that support the purchase and create a fixed asset file. This spending will be needed to determine if you wish to depreciate the purchase over time, take advantage of bonus depreciation, or expense the purchase using code section 179. Your choices create a great tax planning tool.

- Review the impact of COVID-19. There are a number of federal and state initiatives that will need to be considered when filing your 2021 tax return. If you received payroll credits for employee retention or have a Paycheck Protection Program loan that needs to be accounted for this year, be prepared with the details. It will be important to correctly account for these funds.

Ideas to Improve Your Financial Health in 2022

A new year. New resolutions. Here are five ideas to consider to help improve your financial health in the upcoming year.

- Save more for retirement. Plan for the future by feathering your retirement nest egg. For instance, you can contribute up to $20,500 to a 401(k) account in 2022, plus another $6,500 if you’re age 50 or older. Plus, your company may provide matching contributions up to a stated percentage of compensation. And you can supplement this account with contributions to IRAs and/or other qualified plans.

- Update your estate plan. Now is a good time to review your will and make any necessary adjustments. For example, your will may need to be updated due to births, deaths, marriages or divorces in the family or other changes in your personal circumstances. Also review trust documents, powers of attorney (POAs) and healthcare directives or create new ones to facilitate your estate plan.

- Rebalance your portfolio. Due to the volatility of equity markets, it’s easy for a portfolio to lose balance against your investment objectives. To bring things back to where you want, review your investments periodically and reallocate funds to reflect your main objectives, risk tolerance, and other personal preferences. This will put you in a better position to handle the ups and downs of the markets.

- Review, consolidate, and lower debt levels. One sure-fire method for improving your financial health is to spend less and save more. Start by chipping away at any existing debts. This may mean giving up some luxuries, but it’s generally well worth it in the long run. Pay extra attention to debts with high interest charges like credit card debt. If possible, consider consolidating several of these debts into one or two obligations if you can lower your interest rate in the process.

- Contingency planning. No one can foresee every twist and turn that 2022 will take. To avoid potential financial hardship, look to improve your emergency fund by setting aside enough funds to pay for six months or more of your expenses in case of events like a job loss or a severe health issue.

These five tips can help you thrive in 2022!