Happy New Year!

The new year begins with more stimulus payments and other financial assistance courtesy of the latest COVID relief legislation. Read about how the new bill affects your tax and financial outlook.

Also in this month’s edition is good news for business owners regarding the tax deductibility of expenses paid for using PPP loan funds that are forgiven. You can also determine how much to contribute to your retirement fund in 2021 and finds tips on making your 1099 filing go smoother.

Please call if you would like to discuss how this information could impact your situation. If you know someone who can benefit from this newsletter, feel free to send it to them.

More Stimulus Payments on the Way

What you need to know NOW!

You could soon see another stimulus payment in your bank account with the recent passage of the Emergency Coronavirus Relief Act of 2020, which means more direct relief to you and your family. Here are some of the major points you need to know that are buried inside this $900 billion piece of legislation.

Direct stimulus payments to you. The legislation includes a $600 payment per person, including adults and dependent children who are under age 17. Payments are based on your 2019 income and should start being distributed shortly, per Treasury Secretary Mnuchin. The payment amount phases out for adjusted gross incomes over $75,000 for single taxpayers and $150,000 for married couples.

Things to consider:

- If your income in 2019 is over the phaseout threshold, but not over the phaseout threshold for 2020, you will have an opportunity to request the funds on your 2020 tax return.

- Unlike the first round of stimulus payments in 2020, if you have someone in your household who is ineligible, you can still get payments for those individuals who are eligible.

- If the number of adults or dependents in your household changed during the year, you will need to keep track of this and be prepared to issue corrections to ensure you receive the correct payment amount.

- The payment mechanism in place for the initial 2020 direct stimulus payments should help facilitate distributions of this second round of direct stimulus payments.

Extension of unemployment benefits. Federal unemployment benefits of up to $300 per week are extended through March 14. Benefits for self-employed workers, set to expire at the end of 2020, are also extended.

Things to consider:

- If you have not already done so, you must file for unemployment with your state.

- These benefits also apply to self-employed and part-time employees. Many workers who were eligible for this unemployment earlier in 2020 did not file because this class of workers is typically not eligible for most state unemployment programs.

New PPP loan funds. There is additional money available from the Small Business Administration (SBA) for a new round of PPP loans. The new loan program is targeted to businesses that need the funds. To qualify, your business must have 300 or fewer employees and have seen a drop in revenue of 25% or more during any quarter in 2020. Some of the money is earmarked for very small borrowers, underserved communities, and small lenders. There are even simplified requirements for forgiveness if the loan amount being applied for is less than $150,000.

Eviction moratoriums and rent assistance. The bill extends until January 31, 2021 a moratorium on evictions that was scheduled to expire at the end of 2020. The bill also includes $25 billion in emergency assistance to renters.

There is much more in this huge bill, including relief for hard-hit industries, education, student loans, and vaccine assistance. Please keep up-to-date as more is learned after a full review of the bill is made available.

PPP Loan Expenses Are Now Tax Deductible

If you or your business received funds from the Paycheck Protection Program (PPP), the recently passed Emergency Coronavirus Relief Act of 2020 will help to dramatically cut your tax bill. Here’s what you need to know.

Background

The PPP program was created by the CARES Act in March 2020 to help businesses which were adversely affected by the COVID-19 pandemic. Qualified businesses could apply for and receive loans of up to $10 million. Loan proceeds could be used to pay for certain expenses incurred by a business, including salaries and wages, other employee benefits, rent and utilities.

If the business used at least 60% of loan proceeds towards payroll expenses, the entire amount of the loan would be forgiven.

The Dilemma

While the CARES Act spelled out that a business’s forgiven PPP loan would not be considered taxable income, the legislation was silent about how to treat expenses paid for using PPP loan proceeds if the loan was ultimately forgiven.

Congress intended for these expenses to be deductible for federal tax purposes. But since the legislation was silent on this issue, the IRS swooped in and deemed these expenses to be nondeductible.

There was considerable debate over the latter half of 2020, with Congressional politicians explaining that their intent was that the expenses be deductible and the IRS responding “Too bad, they’re nondeductible.”

The Solution

Congress overruled the IRS’s position in the Emergency Coronavirus Relief Act of 2020. The legislation officially makes deductible for federal tax purposes all expenses paid for using proceeds from a forgiven PPP loan.

Stay tuned for updates as to how this new legislation affects your business.

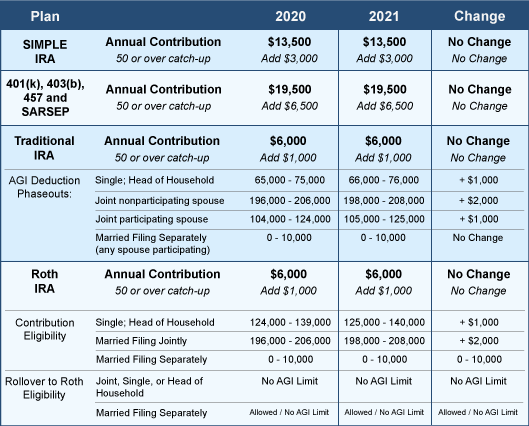

2021 Retirement Plan Limits

As part of your 2021 tax planning, now is the time to review funding your retirement accounts. By establishing your contribution goals at the beginning of each year, the financial impact of saving for your future should be more manageable. Here are annual contribution limits for 2021:

Take action

If you have not already done so, please consider:

- Reviewing and adjusting your periodic contributions to your retirement savings accounts to take full advantage of the tax advantaged limits

- Setting up new accounts for a spouse or dependent(s)

- Using this time to review the status of your retirement plan

- Reviewing contributions to other tax-advantaged plans including flexible spending accounts and health savings accounts

Seven Tips For Financial Wellness In 2021

Common New Year’s resolutions are to lose weight or become more active. Perhaps 2021 is the year to shift focus. Here are seven tips to help you become more financially fit.

- Create a budget. It’s easy to get into financial trouble if you spend more than you earn. By watching your budget more carefully, you might be surprised by how much you spend in certain areas of your life. Many banks and credit unions offer budgeting tools directly on their websites.

- Get a free credit report. You can obtain a free copy of your credit report from each of the three major credit reporting agencies every 12 months. Reviewing your reports regularly can help ensure the data in your report is accurate and allows you to contact creditors to dispute any errors.

- Pay down debt. Start chipping away at your debts through a series of regular payments. Begin with bills that have the highest interest rates. Research whether it makes sense to consolidate debts at a more reasonable interest rate.

- Review your investments. With recent changes in Washington, D.C. and market volatility, reviewing your investments is more important than ever. Protect yourself against risks by diversifying across different classes of investments. If you have not developed an asset allocation plan, do so. If you have, adjust your portfolio to ensure it is still meeting your objectives.

- Plan ahead for retirement. Take advantage of tax-favored retirement plans such as a 401(k) at work. Both the contributions and earnings are tax-deferred and can compound over time. The 401(k) limit for 2021 is $19,500 ($26,000 if you’re age 50 or over). Also consider contributing to an IRA, which has a contribution limit of $6,000 ($7,000 if you’re age 50 or older).

- Check your insurance coverage. Things can change over time, so don’t assume the coverage you acquired years ago still provides adequate protection for your family or business. Take a look at your policies to determine if adjustments are needed.

- Save for emergencies. And finally, would you be financially prepared if your business failed or you lost your job? The COVID-19 pandemic has reminded us the importance of establishing an emergency fund that can last for several months if you lost your salary or business revenue dramatically declines.

Acting on all these tips may seem a bit overwhelming. By focusing on a few now, before you know it, your financial wellness will improve over time.

Make Preparations for Form 1099s This Year

Be looking for new Form 1099-NEC!

Here are three tasks to consider that will make meeting your business’s information reporting requirements less stressful this tax season.

- Review your general ledger. Even if you’ve already identified 1099 vendors in your payables system, review current year expenses to make sure no new or infrequent payments have been overlooked. For example, it’s easy to forget that fees totaling $600 or more paid to service providers must be reported on a Form 1099. But be careful! There is a new form this year, Form 1099-NEC. Be sure to know whether you should use the existing Form 1099-MISC or the new Form 1099-NEC.

- Verify vendor information. Check your files for up-to-date Forms W-9, the form you use to request a vendor’s federal taxpayer identification number (TIN). In general, you should have Form W-9 on file for each vendor who provides services, even if the transaction is a one-time event. Why? Filing mismatched 1099 forms – where the combination of name and TIN do not match IRS records – will result in a notice, and possibly penalties. To avoid problems, consider signing up for the TIN Matching Program, an online service run by the IRS, so you can verify identification numbers prior to filing 1099s.

- Order forms. If you plan to file paper forms this year, the copy you mail to the IRS must be on forms preprinted with scan-friendly ink. You’ll also need Form 1096, the annual summary, for each type of information return you file.

As always, should you have any questions or concerns regarding your tax situation please feel free to call.