Welcome 2020. A new year calls for a fresh look at your financial strategies. Consider how to make the most of your savings accounts — and don’t forget you still have time to fund your IRA! You can also try the following fail-proof tricks to keep your New Year’s resolutions on track.

Call if you would like to discuss how this information relates to you. If you know someone who can benefit from this newsletter, feel free to send it to them.

Make Your Cash Worth More

Banking tips to help you cash in

Your cash is parked. Do you know if it’s making or losing you money? For instance, letting it sit in a non-interest-bearing account is a waste of earnings potential. It’s actually losing money if you factor in inflation! Here are some ideas to help you make the most of your banked cash:

- Understand your bank accounts. Not all bank accounts are created equal. Interest rates, monthly fees, minimum balances, direct deposit requirements, access to ATMs, other fees and customer service all vary from bank to bank and need to be considered. Start by digging into the details of your accounts. There may be some things you’ve been unnecessarily living with like ATM fees or monthly account charges. Once you have a handle on your current bank, conduct research on what other banks have to offer.

- Know your interest rates. As a general rule, the more liquid an account, the lower the interest rate. Checking accounts offer the lowest rates, then savings accounts, which yield lower rates than CDs. Maximizing your earnings is as simple as keeping your cash in accounts with higher interest rates. The overall interest rate earned between all your accounts should be higher than the inflation rate, which is generally around 2 percent.

- Make smart moves. There are a couple of things to take into account when making transfers. First, federal law allows for only six transfers from savings and money market accounts per month. Second, if you invest in longer term investments like CDs or bonds, there are penalties for withdrawing funds before the maturity date. So make sure you can live without the funds for the duration of the term.

- Stay diligent. Putting together a cash plan is just the start. The key to success is to be persistent. Besides losing out on potential earnings, mismanaging your cash can result in hefty overdraft fees. The more attention you devote, the more your money will grow.

There’s Still Time to Fund Your IRA

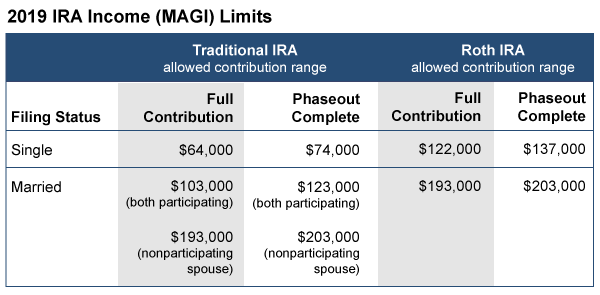

There is still time to make a contribution to a traditional IRA or Roth IRA for the 2019 tax year. The annual contribution limit is $6,000 or $7,000 if you are age 50 or over.

Prior to making a contribution, if you (or your spouse) are an active participant in an employer’s qualified retirement plan (a 401(k), for example), you will need to make sure your modified adjusted gross income (MAGI) does not exceed certain thresholds. There are also income limits to qualify to make Roth IRA contributions.

Maximum 2019 IRA Contribution amounts: $6,000 or $7,000 (with age 50+ catch-up provision)

Note: Married traditional IRA limits depend on whether either you, your spouse or both of you participate in a qualified employer-provided retirement plan. If married filing separate and either spouse participates in an employer’s qualified plan, the income phaseout to contribute is $0-10,000.

If your income is too high to take advantage of these IRAs you can always make a non-deductible contribution to an IRA. While the contributions are not tax-deferred, the earnings are not taxed until they are withdrawn.

2020 Retirement Plan Limits

As part of your 2020 planning, now is the time to review funding your retirement accounts. By establishing your contribution goals at the beginning of each year, the financial impact of saving for your future should be more manageable. Here are annual contribution limits:

Take action

If you have not already done so, please consider:

- Reviewing and adjusting your periodic contributions to your retirement savings accounts to take full advantage of the tax advantaged limits

- Setting up new accounts for a spouse or dependent(s)

- Using this time to review the status of your retirement plan

- Reviewing contributions to other tax-advantaged plans including flexible spending accounts and health savings accounts

Fail-Proof Your New Year’s Resolutions

New Year’s resolutions get a bad rap — and for good reason. They are wildly unsuccessful. Millions of people have well-intentioned aspirations for the new year, but only about one in 10 actually accomplish their goal, according to the Statistic Brain Research Center.

If you dig a little deeper into the reasons why they fail, you find it’s usually not the resolution itself, it’s in the execution. Here are four popular New Year’s resolutions and how to avoid messing them up:

- Resolution #1: Becoming healthier. The most popular resolution can take on many forms — losing weight, getting in better shape, eating healthier, and so on. This resolution usually fails because to be successful, it takes a major lifestyle change. You’re fighting against months or maybe years of poor behaviors, so expecting wholesale changes right out of the gate is not reasonable.Make it fail-proof: Start with smaller, simpler goals like not eating after 8 p.m., or exercising for 20 minutes a day for three times a week. Hitting manageable goals will build momentum and create good habits.

- Resolution #2: Spending less money. Depending on how much you spent on Christmas, this one might take care of itself for a few weeks. But if you don’t have a spending plan or budget, old spending habits will re-emerge.Make it fail-proof: Take some time at the beginning of the year to jot down some long-term spending and savings goals and then work backwards to figure out how those goals will affect your weekly purchases. As the year goes on, continue to track your progress and evaluate your purchases.

- Resolution #3: Getting more organized. Going from being disorganized to organized is not a quick fix. To make the switch, it takes an evaluation of your entire environment. Most people don’t have the time for such an extensive process so they buy some bins, stuff them full and call it good. That’s not going to work and it’ll cost you money.Make it fail-proof: Instead, start small. Pick one room in your house or one aspect of your life to focus on, like health care bills or your tax documents. Once you get some traction, you can apply the methods you learned to other things. Incremental improvement is the best long-term approach.

- Resolution #4: Spending less time on electronics. If this is a resolution that’s important to you, odds are you’ve had some trouble keeping electronic usage under control. With so many games, social media and streaming options at our fingertips, our brains are now conditioned to be engaged electronically at all times.Make it fail-proof: One way to start to break this habit is to change the accessibility you have to your devices. Remove apps from your phone and keep your devices out of reach when you don’t need them. Another way to curb electronic usage is to form a different habit, such as reading.

Resolutions, whether at New Year’s or any other time, are a good thing. To be successful, more planning and attention are required than most people think. And if you slip up, don’t quit! Learn from your mistakes and keeping going.

As always, should you have any questions or concerns regarding your tax situation please feel free to call.

This publication provides summary information regarding the subject matter at time of publishing. Please call with any questions on how this information may impact your situation. This material may not be published, rewritten or redistributed without permission, except as noted here. This publication includes, or may include, links to third party internet web sites controlled and maintained by others. When accessing these links the user leaves this newsletter. These links are included solely for the convenience of users and their presence does not constitute any endorsement of the Websites linked or referred to nor does Wagner Ferber Fine and Ackerman PLLC have any control over, or responsibility for, the content of any such Websites. All rights reserved.