Welcome to tax month! Perhaps welcome is not quite the right word, but to help lighten the mood, included in this month’s newsletter is a fun state tax quiz plus answers to the most common questions taxpayers ask during the month.

Also read about ideas to manage your emergency fund while in our new inflationary environment and a dozen money topics every young person should understand prior to leaving the nest.

Enjoy! Please feel free to forward the information to someone who may be interested in a topic and call with any questions you may have.

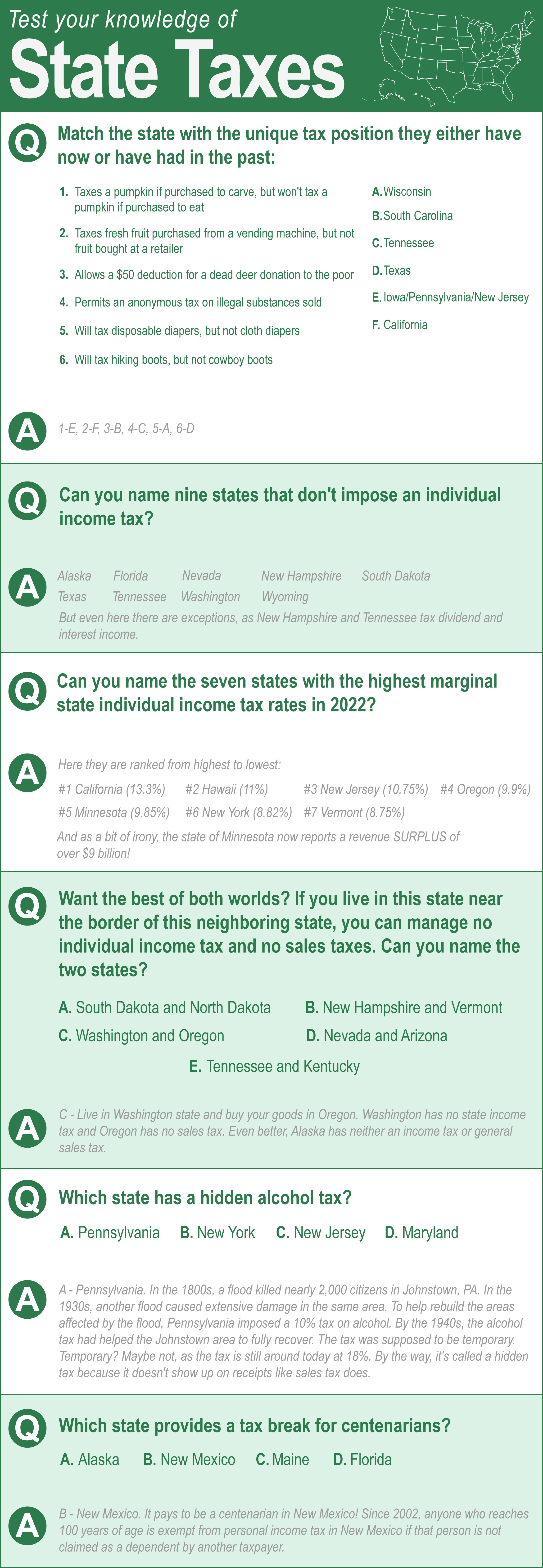

A Fun State Tax Quiz. Go Figure…

A quiz to celebrate April tax month!

With this year’s April tax deadline right around the corner, here’s a fun quiz that explores how states tax their citizens. So you think it’s rough in your state? Try answering the following questions:

Protect Your Emergency Fund From Inflation

Most financial experts suggest keeping three to six months worth of household expenses in savings to help in case of emergency. But with record inflation, that task just got a lot harder to accomplish as virtually every safe place to put your emergency funds will not provide interest rates that keep pace with inflation. But that does not mean you cannot increase the rate of return on these funds.

Here are some ideas to reduce the impact of inflation on your emergency funds.

- Actively monitor your savings account rate. Earlier this year the Federal Reserve increased interest rates for the first time since 2018. In addition, the head of the Federal Reserve is suggesting there may be several of these rate increases in the next twelve months. This should increase the interest you can earn on the cash in your emergency account.

- What you need to know: Not all savings accounts are created equal. When the Fed increases the interest rate, your saving account rate should also go higher…immediately. But this is not always the case. If your bank is slow to raise your savings rate, be willing to monitor and shift funds to a bank that does. Just make sure the funds are still FDIC insured and are kept at a reputable bank.

- Take a look at Series I Savings Bonds. Series I Savings bonds are issued and backed by the U.S. government and feature two interest rate components: a fixed rate and an inflation rate. The fixed rate is set when the bond is issued and never changes during the life of the bond. The inflation rate resets semi-annually based on the Consumer Price Index.

- What you need to know: You must hold an I bond for at least 12 months before redeeming it. And although you can redeem it after one year, you’ll have to pay a penalty worth the interest of the previous three months if you redeem the bond within five years. And remember, you must be prepared to pay the penalty if you need the funds for an emergency.

- Creative use of Roth IRA funds in an emergency. Roth IRAs are funded with after-tax dollars. Because of this, early removal of the initial contribution is tax and penalty free. If you dip into the earnings, however, you will not only be subject to income tax, but also may be subject to a 10% early withdrawal penalty.

- What you need to know: Use of a Roth IRA is often a creative way to fund your emergency account while achieving higher returns with conservative investment choices, but it is not for the faint of heart. If you get this one wrong, it could cost you in taxes, penalties and lost fund value in a bear market. Prior to removing funds from any IRA, it makes sense to conduct a tax planning session.

Please call if you have questions about how to reduce the impact of inflation on your emergency fund.

Common April Tax Questions Answered!

The individual tax deadline of April 18th (yes, this year it’s April 18th!) is fast approaching. Here are answers to five common questions that taxpayers typically ask in April.

- What happens if I don’t file on time?

There’s no penalty for filing a tax return after the deadline if you are set to receive a refund. However, penalties and interest are due if taxes are not paid on time or a tax extension is not requested AND you owe tax.To avoid this problem, file your taxes as soon as you can because the penalties can pile up pretty quickly. The failure-to-file penalty is 5 percent of the unpaid tax added for each month (or part of a month) that a tax return is late. - Can I file for an extension?

If you are not on track to complete your tax return by April 18th, you can file an extension to give you until Oct. 17, 2022 to file your tax return. Be aware that this is only an extension of time to file — not an extension of time to pay taxes you owe. You still need to pay all taxes by April 18th to avoid penalties and interest.So even if you plan to file an extension, a preliminary review of your tax documents is necessary to determine whether or not you need to make a payment when the extension is filed. - What are my tax payment options?

You have many options to pay your income tax. You can mail a check, pay directly from a bank account with IRS Direct Pay, pay with a debit or credit card (for a fee), or apply online for an IRS payment plan.No matter how you pay your tax bill, finalize your tax payment arrangements by the end of the day on April 18th. - When will I get my refund?

According to the IRS, 90 percent of refunds for returns that are e-filed are processed in less than 21 days. You could end up waiting several months, however, if you paper file your return. The IRS is still processing a backlog of several million paper-filed tax returns from last year.You can use the Where’s My Refund? feature on the IRS website to see the status of your refund. The refund information is usually available 24 hours after receiving confirmation that your e-filed tax return was accepted by the IRS. - I hear the IRS is still backlogged with last year’s tax returns. Is this true?

Yes. Late changing tax legislation created tons of extra work for the IRS, all while the pandemic played havoc on staffing. During a testimony made to Congress, the Director of the IRS claims the backlog will be cleared up by the end of the year…assuming no major demands for are made on their resources.

Help Your High School Student Become Money Smart

A dozen great topics!

Often lost in the race to get kids through high school and on to life in the real world are basic financial skills. Here are a dozen financial concepts to consider explaining to your kids before graduating high school.

- How bank accounts work. While there are numerous online applications, consider using a good ol’ check register when teaching the basics of how to track and reconcile bank account activity.

- How credit cards work. Emphasize to your child that credit card spending actually creates a loan. Go through a monthly statement together and show how interest is calculated and stress the need to never carry a balance from month to month by showing how long it takes to pay off the debt with minimum payments.

- Tax basics. When your child receives their first paycheck, walk through their paystub to explain Social Security and Medicare taxes, federal income tax withholdings, and state tax withholdings. If they receive a Form 1099 instead of a paycheck, consider opening a savings account and explain that they will need to set aside a certain percentage of their money to pay the IRS.

- The power of a retirement account. Explain the advantages of long-term savings tools like an IRA. The wise saver can turn into a self-made millionaire by starting their retirement savings at a young age.

- How credit scores work. Consider explaining how credit scores work and the importance of keeping their score at the highest level possible. If your child is like many young adults who currently doesn’t have a credit score, consider downloading your own credit report and walk through it with them.

- Spend within your means. Saving first before spending is a simple concept that is becoming a lost art. Help your child understand this by setting their sights on something they want, and then help them save money to buy it.

- The art of saving. Part of spending within your means implies that your child has healthy savings habits. Walk your child through the techniques that work for you. Perhaps it is setting up a separate savings account or automatic transfers from a paycheck.

- The strength of investing. The most valuable investment a young person can make is in themselves. Whether it’s a college degree or a trade school diploma, your child can build tremendous value with skills that will provide a positive financial return each year.

- Understanding of stocks and mutual funds. With an understanding of investments, consider teaching your child some of the basic investments available to them. Stocks and mutual funds are the most common, but also consider explaining bonds, CD’s, annuities and other investments.

- Budgeting. Help your child create a basic budget, then help them track their savings and spending against this budget.

- Cash flow. The hard way to learn the lesson of cash flow is when bill collectors are calling and there simply isn’t money to pay them. When creating an initial budget, show your child the flow of funds each month.

- Calculation of net worth. Assets (what you own) minus liabilities (what you owe others) equals net worth. Every person has a net worth…even a child. So help them understand theirs and periodically calculate it.