Our last article on the NY Pass Through Entity Tax (“PTET”) included a lot of “we’re waiting for guidance from the state”, but since then New York has answered most of the burning questions that we had on the PTET. If you are looking for a walkthrough on how to make the election on the NYS website, skip down to the bottom. Let’s review:

What is the NYS PTET?

It is an optional tax, paid for by a pass through entity (like a partnership or S-Corporation), on the entity’s New York income. The entity pays the tax, gets to deduct it (as an ordinary and necessary business expense like any other), and passes the owners of the entity a credit against their New York personal income taxes equal to their share of the tax paid. In other words, the entity pays the tax on behalf of its owners.

Why is it important?

By having the entity pay the tax instead of the individual owners, you are ensuring that you are able to deduct (i.e. offset) the tax paid to the state against your taxable income (the base on which your federal income taxes are calculated). If you opted out of the PTET and opted to have the owners pay the state taxes directly, the owners’ deduction of the state taxes would be limited by the $10,000 SALT cap and would likely not benefit them at all. We went into this in more detail in our last article, so check it out for a refresher.

What are the highlights?

Which of an entity’s shareholders are eligible for a PTET credit to be passed to them by the entity:

Article 22 taxpayers, which includes individuals, trusts, and estates. It does not include partnerships or corporations.

How to actually, physically, make the election to opt into the PTET:

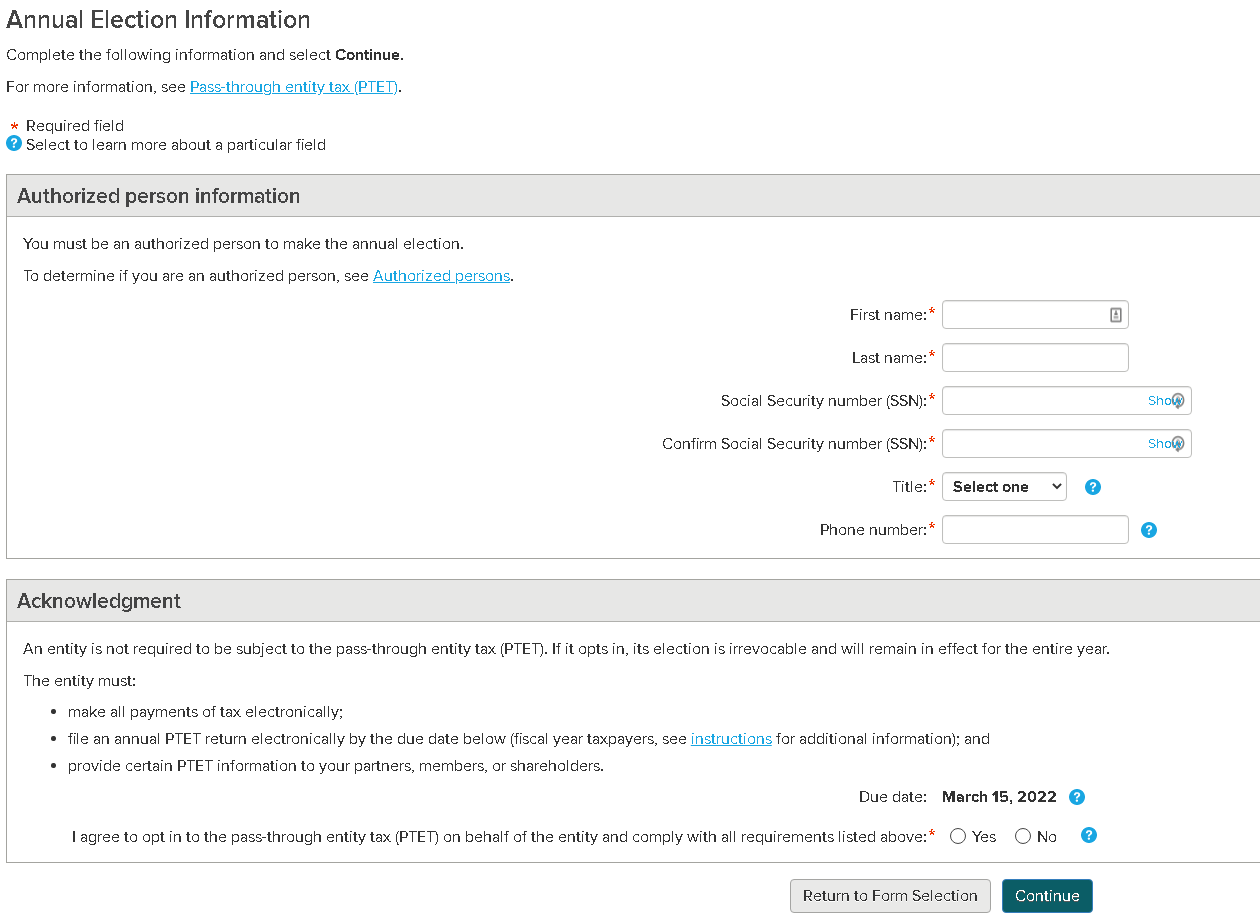

The election must be made by an authorized person of the entity. This means that your accountant cannot make this election for you. An authorized person includes an owner, officer, manager, or individual with authority to sign the entity’s tax return.

The election must be made on the New York State website using the entity’s Business Online Services Account. If your entity does not already have a Business Online Services Account you should create one ASAP, as there are certain circumstances that can lead to delays (sometimes of weeks or even months) in registering the account, and no account means no PTET election.

See below for a detailed walkthrough of how to make this election on the New York website.

When must the election be made?

The election is made annually, and once it is made for a given year it cannot be revoked. For the current year (2021) the election must be made prior to October 15th, 2021. Going forward (starting with 2022) the election must be made by March 15th of that year (e.g. for 2022 the election must be made by March 15, 2022).

What is the PTET based on? How is “PTET Taxable Income” calculated?

The calculation is different for S-Corps and partnerships.

For S-Corps:

- Aggregate any income, gain, loss, or deductions that flows through to direct Article 22 shareholders (read: individuals, trusts, and estates that have a direct ownership in the entity)

- Apportion the net amount of the taxable income to New York based on standard apportionment rules (i.e. NY sales as a % of total sales)

For Partnerships:

- Classify all direct Article 22 partners (read: individuals, trusts, and estates that have a direct ownership in the entity) as residents or nonresidents of New York. For the purposes of this breakdown a partner is treated as a resident of they are considered a resident for personal income tax purposes for at least half of the year. Partners who are trusts are classified based on the residency status of the trust itself, not that of the beneficiaries

- Compute a resident PTE taxable pool

- Compute a nonresident PTE taxable pool

- Aggregate the resident and nonresident PTE taxable pools. Note that the calculation of the taxable pools must take any special allocations into consideration

I’m used to paying my New York estimated taxes personally. How do estimated taxes work for the PTET?

The entity is not required to make any estimated PTET taxes for 2021. Beginning with 2022 the entity (assuming it opts into the PTET) is required to make estimated tax payments, which are due 3/15, 6/15, 9/15, and 12/15. The state has not yet issued the forms to make the payments, but they’ve indicated that they’ll be available in December. Note that entities will want to make the payment in December of 2021 in order to get the deduction this year.

Important Note! For 2021 (only), owners of entities that opted into the PTET are still required to pay their personal estimated taxes to New York as they had in the past to avoid penalties/interest or having an extension disallowed.

What does an individual do with the PTET credit they receive?

Individuals will include the credit on their personal New York income tax return using Form IT-653 (which has not yet been released). The individual must also add the amount of the credit back to their NY income (as an “addition modification”) as New York state taxes are not deductible on the New York tax return.

How does the NY PTET interact with other states’ PTETs?

New York has indicated that resident owners will be allowed resident tax credit against their New York State personal income tax for any PTET imposed by another state as long as the other state’s PTET is “substantially similar” to New York’s PTET. New York plans to release a list of “substantially similar” PTETs, so you won’t have to guess. Check out this article for a quick refresher on the resident credit.

In conclusion…

If you think you may want to make the PTET election for your entity for 2021, now is the time to get the ball rolling. Set up your account on the New York website and make sure that you’re ready to make the election once you’ve decided to proceed.

Not sure if the election is right for your company? We can help you analyze your tax situation to see if this election makes sense for you. Reach out today to schedule a consultation!

How to Make the PTET Election on the New York Website: A Walk Through

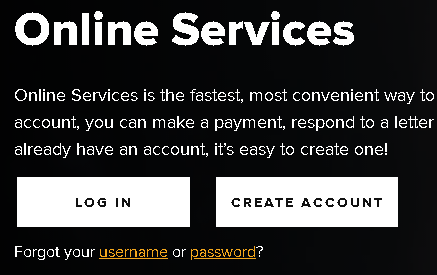

1) Go to https://www.tax.ny.gov/online/

2) Click “Log In” or “Create Account” (if you don’t already have an account for this entity. Note that you may be required to verify your identify when creating a new account by supplying information from a recently filed sales or payroll tax return, so it would be helpful to have these on hand when creating your account for the first time. If you don’t have either you should have your company’s tax ID (EIN) and exact name ready to enter.)

3) Once logged in, click “Services” in the top left

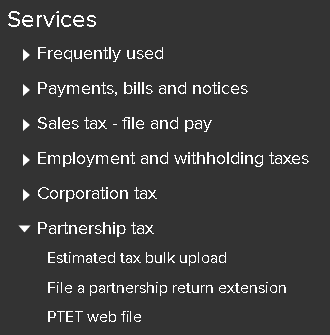

4) Expand “Partnership tax” or “S-Corp Tax” and select “PTET Web File”

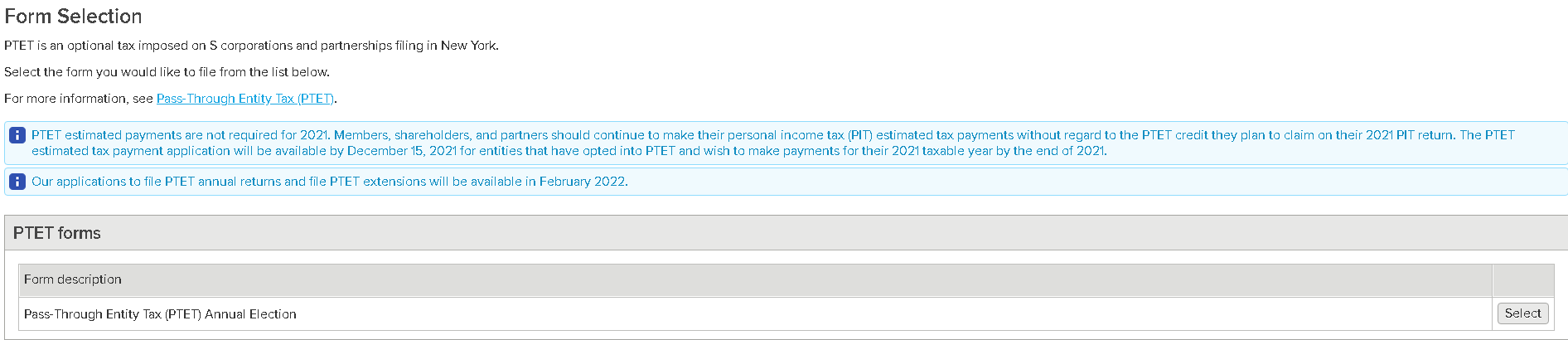

5) Click the “Select” button to the right of “Pass Through Entity Tax (PTET) Annual Election

6) Enter the required information, select “Yes”, and click “Continue”

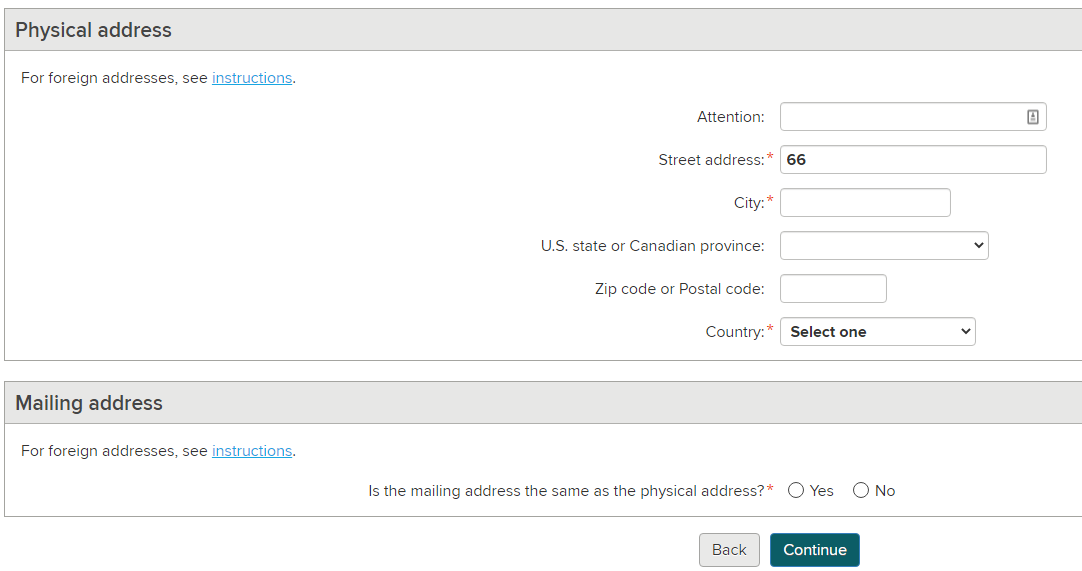

7) Enter the requested address info about your business and click “Continue”

8) Confirm that the information you entered is accurate and click “Submit”

9) Print a copy of the election and send it to your accountant to keep on file

Disclaimer: The topics discussed in this article are complicated, nuanced, and dynamic. Please always consult your tax advisor before taking action.