A 20% Deduction on Income from Pass-Throughs

The new tax law, the Tax Cuts and Jobs Act of 2017, has forced us to change the way we think about many aspects of the tax code, one of the most important of which is the 20% deduction for Qualified Business Income (“QBI”) for pass-through entities. While it may sound simple, in reality, the limitations and criteria that the law applies to this deduction leave things far from simple, especially for tax planning. That said, let’s try to break it down into plain English…

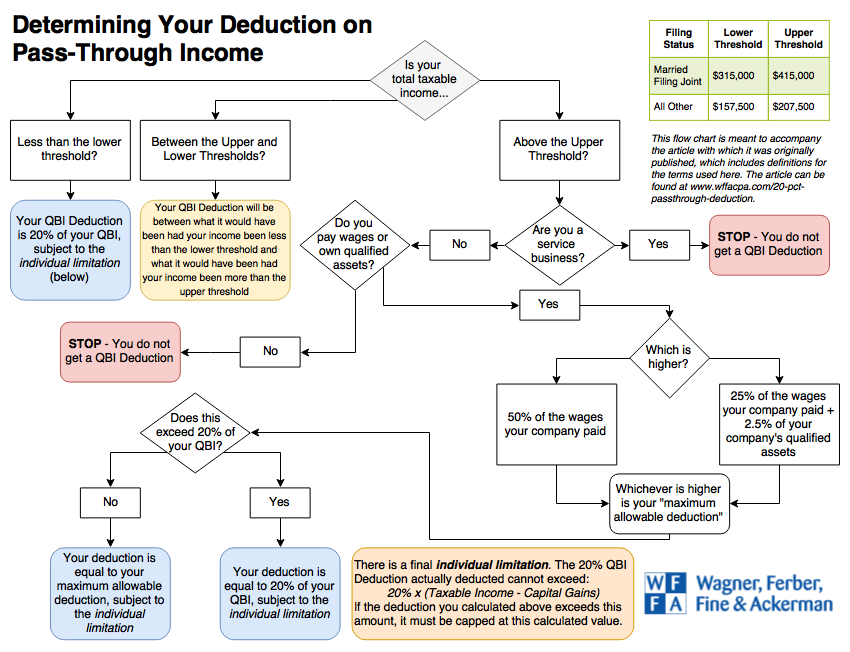

First, a Flow Chart…

If this seems like gibberish, read on! All of the terms used in this flow chart are defined and explained below.

What is the 20% Deduction?

At the most basic level, it is a deduction, taken on your personal tax return, equal to 20% of the Qualified Business Income from pass-throughs that you report on your personal return.

In the past, deductions came in two flavors:

- An adjustment to Adjusted Gross Income (“AGI”), which you’ll sometimes hear referred to as an “Above the Line” deduction

- An itemized deduction, which is sometimes referred to as a “Below the Line” deduction

Generally speaking, adjustments to AGI are better because they decrease your AGI, and a lower AGI makes it more likely that you’ll benefit from certain tax credits or deductions.

To keep things simple (not really), the 20% QBI deduction is not an adjustment to AGI or an itemized deduction, it’s a new type of deduction that is somewhere in between the two (literally, it is between the two lines on the form). It won’t decrease your AGI (which is bad, because a lower AGI is helpful), but you will get to take the 20% QBI deduction even if you don’t itemize your other deductions. So, it’s also figuratively in between the two traditional deduction types with regards to how beneficial it will be.

What do I have to have or do to get this deduction?

First, you have to have Qualified Business Income, which is income from a pass-through entity that is reported on your personal tax return. Pass-through entities include:

- Sole proprietorships and/or single-member LLCs

- Partnerships and/or multi-member LLCs

- S-Corporations

If you have QBI, you then have to figure out if you qualify for the deduction and, if you qualify, whether or not your deduction is limited by certain factors.

An Interjection – Total Taxable Income Below the Threshold

If your total taxable income on your personal tax return is below the threshold, you qualify for the full 20% QBI deduction without having to meet any of the other criteria or having to worry about your deduction being limited or capped. The total taxable income thresholds (depending on your filing status) are:

- Married Filing Joint – $315,000

- Single, Head of Household or Married Filing Separate – $157,500

Continuing – Taxable Income Above the Threshold

If your total taxable income on your personal return is not below the relevant threshold, your 20% QBI deduction may be capped or disallowed entirely.

The Service Business Test

Is your business considered to be a service business?

- Yes – Your 20% QBI deduction is disallowed, sorry (unless you’re under the income threshold mentioned above, in which case your deduction is safe)

- No – Your 20% QBI deduction is safe (for now), move on to the next set of criteria to see if it is limited or capped

What qualifies as a service business?

- The performance of services in the fields of health, law, accounting, actuarial science, performing arts, consulting, athletics, financial services, or brokerage services, or

- The performance of services that consist of investing and investment management, trading, or dealing in securities, partnership interests or commodities, or

- Any trade of business where the principal asset of the business is the reputation or skill of an employee or owner (Note – this third definition casts a very broad net!)

Noteworthy Exception – Architects and engineers, despite being service businesses, are specifically categorized by the law (for the purposes of this deduction) as a non-service business.

The Wage and Asset Limitations

The next hurdle to clear when claiming your 20% QBI deduction is to determine if it is capped or limited. You can measure the limitation in two different ways, and then use whichever one is more beneficial to you (i.e. whichever is higher).

- 50% of the company’s total wages

- 25% of the company’s total wages plus 2.5% of the company’s qualified assets

Questions You’re About to Ask:

- What is included in wages for this calculation? All wages paid to employees and to owners (of an S-Corp)

- What is excluded from wages for this calculation? Guaranteed payments to partners in a partnership

- What are “qualified assets”? Qualified assets are real or personal assets (read: tangible assets like buildings, furniture, computers. Not intangible assets like licenses, patents or good will)

- What value do I use for the assets? You use the original, unadjusted basis of the asset. In most cases, this is equal to whatever you paid for the asset and should not take into account depreciation (Note – 179 depreciation taken does decrease the unadjusted basis of the asset, so this may affect your decisions going forward as to whether to take 179 depreciation or bonus depreciation)

- How many years can I use a qualified asset for? You can use a qualified asset for the “useful life” of the asset (“useful life” for various types of assets are already defined in tax law, for example, a residential property has a life of 27.5 years) or 10 years, whichever is longer (meaning that a desk, which may have a useful life of 7 years, can still be used for this calculation for 10 years)

I have some wages and/or assets, now do I get the QBI Deduction?

Yes! You can now take your 20% QBI deduction, but it must be capped at the limitation you calculated above. For example, if your 20% deduction came to $100,000 before any limitation, and your total wages were $60,000 and you had no assets, your QBI deduction will be capped at 50% of these wages, or $30,000.

A Final Limitation (yes, another one)

If you’ve made it this far, you have one more hurdle to pass that may limit the size of your QBI deduction. Your QBI deduction is limited (again) at to 20% of your (Taxable Income minus Capital Gains). For example, if your 20% deduction (after the wage limitation) came to $25,000, you would now have to compare this to:

20% x (Taxable Income – Capital Gains) = Limiting Factor

If your taxable income is $120,000, which includes $20,000 of capital gains, your limiting factor would be:

20% x ($120,000 – $20,000) = $20,000

This $20,000 limiting factor is lower than the wage-limited QBI deduction above (which was $25,000), so your actual QBI deduction will be shown on your tax return as a $20,000 deduction.

A few miscellaneous notes:

- If you own less than 100% of the entity in question, all of the items above are prorated based on your ownership percentage

- The taxable income threshold is not a hard cut-off, the limitations phase-in when taxable income is between $315,000 and $415,000 for taxpayers filing joint returns and between $157,500 and $207,500 for everyone. If you are in between the upper and lower threshold, your actual deduction will be somewhere in between what it would have been if your income was below the lower threshold and what it would have been if your income was above the upper threshold

- If you are an owner in multiple pass-through entities, you cannot aggregate wages or asset ownership between these entities. So, if you are in a position where you have one entity that pays a lot of employees and has a lot of wages, and another entity that has high income but no payroll (maybe they pay a management fee to the first company), you may be missing out on some or all of the 20% QBI deduction. For taxpayers in this situation, there is an opportunity to do some planning and/or restructuring to maximize your tax savings with regards to this deduction – Update (11/5/18): regulations issued by the IRS after the original publication of this article have allowed for trades or businesses meeting certain criteria to be aggregated. Our article on this topic goes in-depth on what it takes to aggregate.

- Update (1/23/19): The IRS released guidelines for a safe harbor to help determine if a rental real estate enterprise qualifies as a trade or business for purposes of claiming the 20% deduction. For more info, check out our article breaking down the safe harbor.

Is your head swimming?

That’s okay, we’re here for you! Want to walk through how this applies to your tax situation? Considering restructuring your business to maximize your tax savings? Not sure if you’re in a service business? Give us a call, we can help!

As always, whether it’s us or someone else, you should always consult your tax advisor to review your specific situation before taking any action.